March 16, 2026

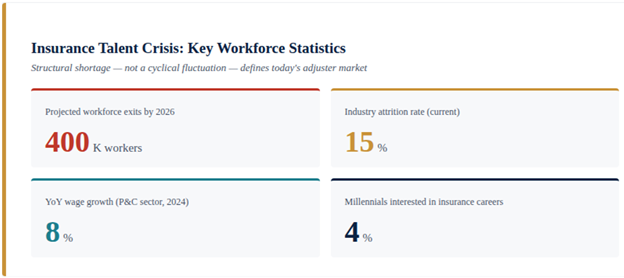

Claims adjusters play a critical role in determining claim outcomes, cycle time, and customer experience. While adjuster fees represent a relatively small portion of total claims payouts, adjuster availability, capability, and performance have an outsized impact on overall claim economics. As insurers face tightening labor markets and increasing claim complexity, the risks associated with adjuster sourcing and management have become more pronounced.

Rising Adjuster Costs and Capacity Constraints.

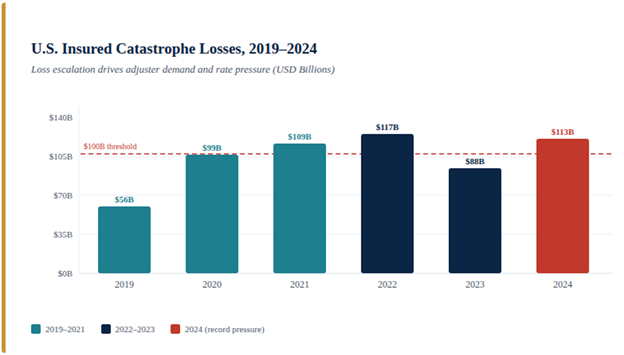

Adjuster labor markets are under sustained pressure. Increased catastrophe frequency, higher credential requirements, and competition for experienced talent are driving up adjuster rates, particularly in specialized lines and high-severity claims. During catastrophe events, surge and CAT adjusters command premium pricing that can distort baseline rate expectations and complicate long-term vendor negotiations. Although these fees remain a small share of total claim costs, limited access to qualified adjusters can delay resolution, reduce accuracy, and increase downstream expenses.

Quality Risk from Underqualified or Underpaid Adjusters.

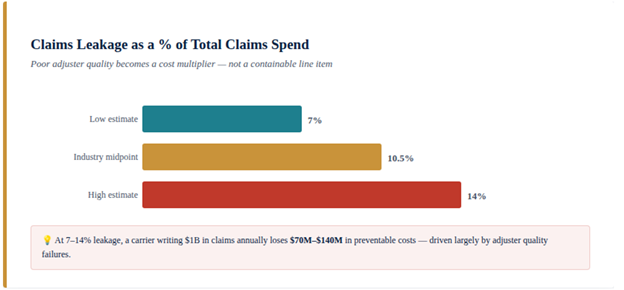

When adjusters lack sufficient expertise or are incentivized to prioritize speed over diligence, claim quality suffers. Inaccurate scoping, inconsistent coverage interpretation, and incomplete investigation increase claim leakage and rework. Overly aggressive fee compression may reduce short-term costs but often leads to rushed assessments and higher downstream costs, including reopened claims, disputes, and litigation. In this context, poor-quality adjusting becomes a multiplier of cost rather than a controllable expense.

Operational Inefficiencies.

Many insurers manage fragmented adjuster ecosystems, with inconsistent rate cards, duplicative vendor rosters, and manual onboarding processes. Procurement and claims teams often operate in silos, resulting in misaligned objectives and limited shared visibility into vendor performance. Without standardized performance metrics or integrated systems, insurers struggle to distinguish high-performing adjusters from underperforming ones, weakening both sourcing and oversight decisions.

Embedded Conflict of Interest.

A structural tension exists in claims operations: insurers seek to control indemnity, while adjusters paid by the insurer determine claim value. Excessive fee pressure may unintentionally incentivize speed over accuracy, undermining fairness and defensibility. Effective governance frameworks are required to preserve adjuster independence, ensure ethical decision-making, and maintain trust with regulators and policy holders alike.

Competency-Based Hiring and Qualification Standards

Financial institutions should mandate active state licenses (NIPR-verified) and recognized professional designations (e.g., AIC, CCP, SCLA), embedded directly into RFQs and approved vendor panels. Adjuster capability must be aligned to claim severity. High-severity or complex claims, including litigated exposures and liabilities exceeding $100K require adjusters with five or more years of experience and proven litigation handling. Routine retail banking or personal lines claims can be allocated to Tier 2 adjusters. Historical performance and compliance records should be screened using objective metrics such as claim leakage (<5%), complaint ratios, and regulatory findings, with volume allocation favoring consistently high-performing vendors.

Structured Adjuster Pools and Assignment Models

Leading bancassurance groups deploy tiered adjuster pools covering CAT events, high-severity files, and routine claims. CAT and surge capacity ispre-contracted through multi-year frameworks, often covering 200+ adjusters,with service-level agreements requiring sub-24-hour response for bank-critical assets. To mitigate concentration risk, institutions cap single-vendor volumes at 25–30% per region while maintaining multiple backup providers. Surge readiness plans include rapid onboarding, guideline training, and early quality checks to preserve claim outcomes during peak loss periods.

Performance Monitoring and Quality Assurance

Claims platforms provide continuous monitoring of core KPIs, including time-to-contact (<24 hours), cycle time benchmarks, reopen rates, supplement frequency, and reserve accuracy. Structured quality assurance programs review 5–10% of files per adjuster quarterly, assessing estimate accuracy and documentation standards. Outliers trigger targeted coaching, while persistent underperformance results in removal from panels. Quantitative scorecards are complemented by qualitative QA reviews and customer experience measures to guide renewals and volume steering.

Ethics and Independence Safeguards

Clear governance frameworks reinforce impartiality, fair indemnity, and Treating Customers Fairly principles. Commercial negotiations are kept separate from coverage and settlement decisions, overseen through joint procurement–claims governance. Incentives reward compliance, accuracy, and customer outcomes rather than payout minimization, with ethics violations resulting in immediate de-paneling.

Co-Building the Commercial Strategy with Claims

Procurement and Claims need to come to a table and jointly develop the commercial strategy before procurement engages the vendor for price discussions. Claims must specify the minimum quality standards, service levels and geographical coverage requirements while procurement designs rate-tiers and consolidates vendors to reduce fragmentation in the vendor base and increase leverage.

Negotiating for Value, Not Just Price

Negotiations must be focused on value, and not just on unit cost. Over-negotiation could lead to disengagement of skilled adjusters and degradation of claim quality while under-negotiation might enable rate inflation and loss of efficiency. We have witnessed commercial models – such as blended fees and outcome linked incentives help align adjuster economics with accuracy, speed and cost control.

Governance and Risk Controls

Procurement and Claims must jointly own governance of the vendor panel rather than treating it as a one-time sourcing event. A standing review forum with clear cadence should track performance against SLAs, drive disciplined rate reviews, and make evidence-based decisions on panel expansion, consolidation, or exit. Standardizing fee schedules, onboarding steps, and compliance controls across vendors reduces operational variance and helps ensure that basic hygiene-licenses, indemnities, data security, and file documentation does not become a source of claims or regulatory risk.

Operational and Customer Outcome Benefits

Structured governance is only useful if it translates into better outcomes for customers and the P&L. When Procurement and Claims align on vendor selection, pricing models, and oversight, adjusters are better positioned to produce accurate estimates, reducing leakage and downstream litigation exposure without slowing cycle time. Consistent quality and communication from adjusters improve policyholder experience and strengthen the carrier’s position with regulators and courts, turning vendor management from a pure cost exercise into a lever for trust, advocacy, and long-term brand equity.

Effective claims management requires more than controlling line-item costs, it demands a disciplined balance between adjuster economics, claim quality, and operational governance. While adjuster fees represent a small portion of total claim spend, adjuster capability and performance materially influence loss outcomes, customer experience, and regulatory defensibility. Insurers that align procurement and claims around shared quality standards, data-driven performance oversight, and thoughtful negotiation are better positioned to manage this balance. By treating adjuster sourcing and governance as a strategic capability rather than a transactional function, insurers can control total claim cost while preserving fairness, consistency, and trust across the claims lifecycle.